On 16 April 2025, Directive (EU) 2025/794 was published, postponing the deadlines for the application of the directives on sustainability reporting (CSRD) and due diligence (CSDDD), under the ‘Stop the Clock’ mechanism. Part of the ‘Competitiveness Compass’ and the Omnibus Package, this measure aims to simplify rules, reduce administrative burdens and strengthen competitiveness without compromising the objectives of the European Green Deal. Among the main changes, the application of the CSRD to large companies with fewer than 500 employees has been postponed to 2027 and to 2028 in the case of SMEs, while in the CSDDD only the largest companies have seen the deadline postponed to 2028. The new Directive must be transposed by 31 December 2025.

On 16 April 2025, Directive (EU) 2025/794 of the European Parliament and of the Council was published, which amended the dates for the application of certain corporate sustainability reporting requirements and the requirements for companies’ sustainability due diligence.

This Directive, which concerns the suspensive mechanism known as the "Stop the Clock mechanism", amended the directives on corporate sustainability reporting (CSRD) and companies’ sustainability due diligence (CSDDD or CS3D), only with regard to the respective deadlines for application to companies within their scope.

The proposal to postpone the entry into force of the CSRD and the CSDDD comes within the scope of the European Commission’s "Competitiveness Compass", which aims to reconcile the sustainable transition with strengthening the competitiveness of European Union (EU) companies. After the entry into force of both Directives, stakeholders considered that implementing the obligations on sustainability and due diligence reporting would be too complex and costly, and would overall harm the competitiveness of companies and investments in the EU.

To this end, through the Omnibus package (which includes the stop the clock mechanism), the Commission has simplified the rules for reporting on sustainable financing, sustainability due diligence, EU taxonomy, the carbon border adjustment mechanism and Europe's investment programmes, reducing administrative burdens for companies by at least 25% and for SMEs by at least 35%.

In this way, by focusing compliance with sustainability obligations on companies with the greatest climate impact, the overall objective of the Omnibus package is to simplify the regulatory framework, reduce bureaucracy and reduce costs (which are expected to save around EUR 6.3 billion per year) without, at the same time, compromising the European Green Deal’s objectives for a green and fair transition.

The aim of this postponement is to give the relevant institutions more time to agree on the most substantial amendments to be made to these two directives in order to streamline and simplify their rules, reduce the reporting burden and enhance competitiveness.

The published Directive has already entered into force and must be transposed into national law by 31 December 2025.

Below is an explanatory table of the main changes regarding the dates for application of the requirements set out in the CSRD and the CSDDD:

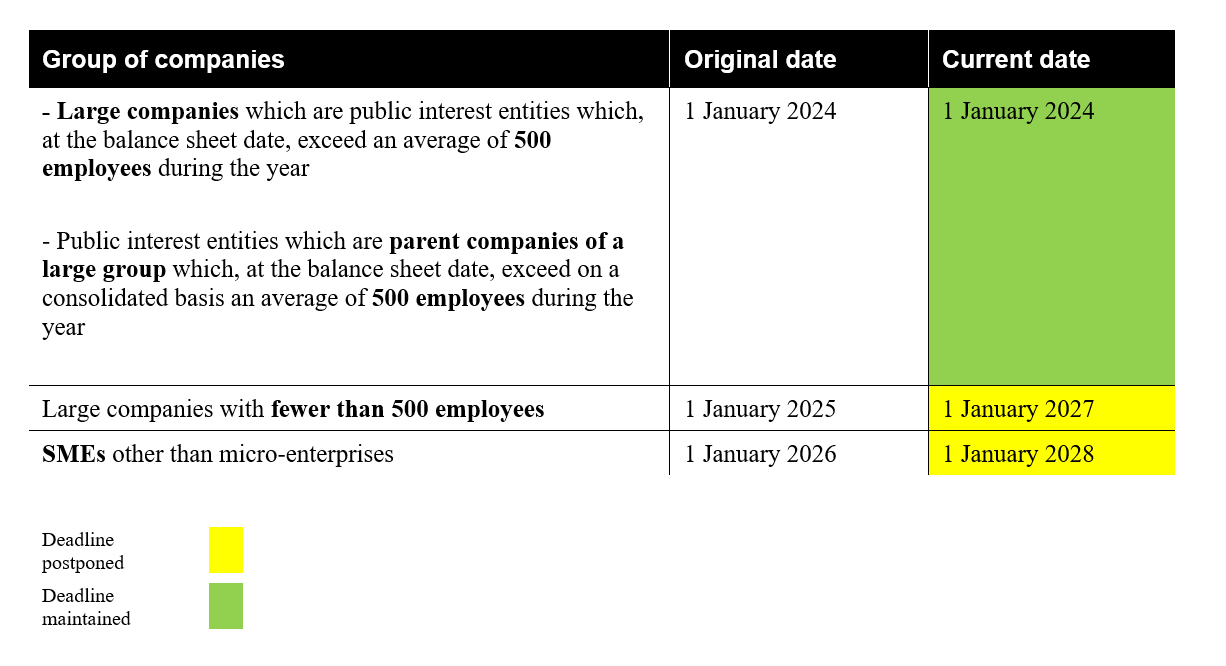

CSRD - Corporate sustainability reporting

Date after which sustainability reporting requirements should apply to companies:

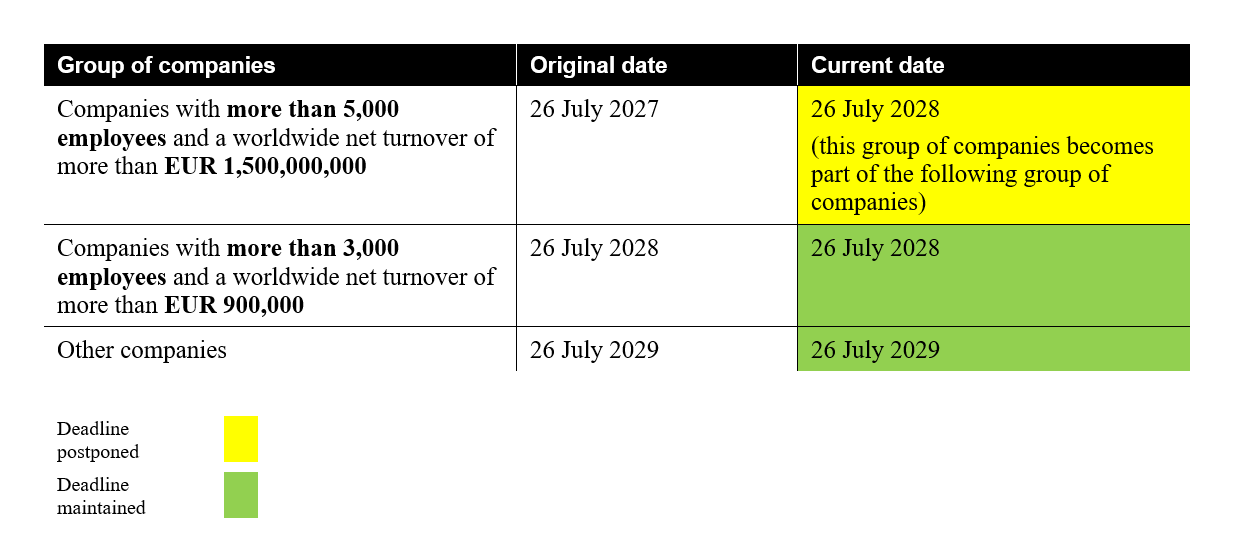

CSDDD - Corporate sustainability due diligence

Date from which the due diligence requirements should apply to companies:

The deadline for transposition of this Directive is also postponed from 26 July 2026 to 26 July 2027.